March 11, 2026

Trump Accounts: An Overview and Comparison

Trump Accounts are generating significant interest across the financial planning community and among clients with young children or grandchildren. Created under the One Big Beautiful Bill Act (OBBBA) and codified under IRC Section 530A, these new savings vehicles represent a novel, and still evolving, option for building wealth on behalf of minors. The following is an objective, educational overview of what we currently know about Trump Accounts, what remains unclear and how they compare to two more established savings alternatives – 529 Savings Plans and Uniform Transfers to Minors Act (UTMA) accounts.

What Are Trump Accounts

Trump Accounts are tax-deferred savings accounts for children, created by the OBBBA and available starting July 4, 2026. Any child under the age of 18 who has a valid Social Security number is eligible to open an account. The account is owned by the child but administered by a parent or guardian until the child turns 18. Contributions may come from a variety of sources including parents, grandparents, other individuals, employers, government entities and tax-exempt organizations. Only one funded Trump Account is permitted per child.

The primary centerpiece of Trump Accounts is the federal government’s one-time $1,000 “seed” contribution for U.S. citizens born between January 1, 2025, and December 31, 2028, provided a tax election is filed on the child’s behalf. Children born outside that window are still eligible to open an account; however, they simply will not receive the seed contribution.

What We Know

Key rules and mechanics we have a reasonable understanding of are:

- Contributions: Annual contributions are capped at $5,000 (indexed for inflation starting in 2027) per child and does not include the $1,000 seed contribution. Multiple sources can contribute annually, the most common likely to be after-tax contributions from individuals (parents or grandparents) and contributions from employers. Employers may contribute up to $2,500 per employee per year (counting toward the $5,000 maximum), either through direct employer contributions or employee pre-tax salary deferrals through a benefits plan. Importantly, the child does not need to have earned income to receive contributions, a key distinction from Traditional and Roth IRA savings plans.

- Investments: Investment options within Trump Accounts are intentionally limited. Funds must be invested in low-cost index mutual funds or exchange traded funds that track the S&P 500 or another qualifying U.S. equity index, with at least 90% of holdings in U.S. companies. This structure prioritizes simplicity and low-cost investment vehicles.

- Withdrawals: Withdrawals from the account are generally prohibited before the year the child turns 18. After age 18, the account is treated like a traditional IRA, meaning distributions before age 59 and ½ are mostly taxable as ordinary income and subject to a 10% early withdrawal penalty, with limited exceptions.

- Tax Considerations: Tax treatment depends heavily on the source of contributions. Individual (after-tax) contributions are not taxable when withdrawn, but earnings always are. Pre-tax employer and employee salary deferral contributions are fully taxable upon withdrawal as is the government seed contribution when distributed. This emphasizes the importance of keeping accurate records of Trump Accounts once established.

What We Still Need to Understand

While the legislative framework is in place, important details still need to be clarified by the IRS. Areas we are closely monitoring are:

- Gift Tax Treatment: Whether contributions from individual donors will trigger federal gift tax filing requirements is unknown. If contributions are treated as “future interests,” donors may need to file gift tax returns and may use lifetime exemption, a potentially significant concern.

- Roth Conversions: It is unclear whether the account owner may convert their Trump Account to a Roth IRA at age 18. Such a conversion would be highly beneficial, enabling decades of tax-free growth.

- Management Logistics: The IRS is still developing the approved list of investment options, and clarification is still needed on how the parent or guardian may be able to transition the account from an initial custodian chosen by the US Treasury to other providers.

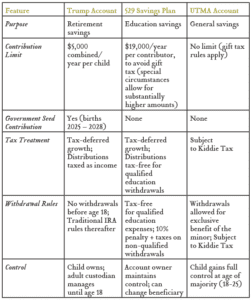

Comparing Trump Accounts, 529 Savings Plans, and UTMA Accounts

Each savings vehicle serves a different purpose and carries distinct advantages and limitations. The table below provides a high-level, side-by-side comparison across the most important features of the three savings vehicles.

Conclusion

Trump Accounts represent a new and noteworthy tool in the child savings landscape, and the $1,000 seed contribution is an opportunity that eligible families should not overlook. However, they are not a replacement for existing vehicles. For families focused on education savings, a 529 savings plan remains the gold standard, offering superior tax benefits, greater contribution flexibility and parental control. For families seeking general savings without restrictions, an UTMA may be appropriate, with the understanding of its limitations. Trump Accounts may best serve as a complement to these existing strategies, particularly for long-term, retirement-oriented savings for a child. As always, the right combination depends on each family’s specific goals, tax situation and time horizon.