August 13, 2019

The Doom Loop

When I first began dealing in global bonds and currencies in the mid-eighties, one of my most experienced clients, a mainstay on the London asset management scene, told me in the quiet conspiratorial tone that the Brits often use to cut people to the quick without really being explicit, “John, never buy bonds of countries which have green in their flag.”

Today, of course, he would be accused of gross Islamophobia since most Islamic countries have green in their flag, but in the late eighties he was really talking about Italy where countless governments, unpredictable budgets and constant capital flight meant that until the mid-nineties, Italian bonds were the most unreliable of investments in the European government bond universe. My friend did eventually invest in Italy when the country initiated a reform process designed to get them into the Euro. However, once in, the Italians have consistently proved a thorn in the side of the European experiment and global bond managers. In fact, Central Banking institutions and portfolio managers in Europe have begun to talk about something called The Doom Loop with regards to Italy, its banking system and its potential for contagion in the European banking system.

The doom loop is the circle of vulnerability where a country’s banking system can be severely hurt by volatility in the price of the sovereign bonds they hold for reserves resulting in a contraction in lending provided by the banks. This contraction in credit, in turn, slows the domestic economy, resulting in a further deterioration in the price of the sovereign’s bond issues as the government is forced to increase its borrowing to maintain services in a period when tax receipts are falling. The loop can also begin with the banking sector if a contraction in bank lending due to liquidity or non-performing loan problems sparks volatility in the government bond prices by slowing the economy and eroding confidence in the sovereign credit. The circle can also be activated by external forces such as a slowdown in global economic activity due to natural recession or trade friction as well as, in the Italian case, a change in the provision of liquidity to the financial system by its external fiscal and monetary partners i.e., the EU or the European Central Bank (ECB). Going the other way in the circle, an Italian bank failure or a blowout in the sovereign spread can adversely affect foreign holders of Italian debt, particularly European banks.

To understand the current situation in Italy, let’s look in more detail at these moving parts.

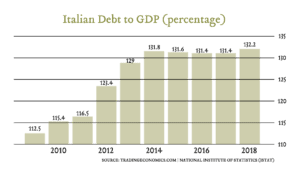

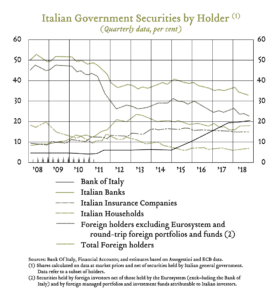

Italian government debt is large and growing. The country’s debt to GDP ratio is 132% as opposed to a Euro area average of 86% and is exceeded in Europe only by Greece whose debt to GDP is 182%.1 Since Italy does not control its own money supply, she cannot print money to meet these debts nor can she devalue her currency to boost her economy (her favourite pre-Euro trick). Moreover, the country’s debt is largely owned by two groups. First, of the €2.3 trillion of public Italian debt, the Italian banking system owns 30%, a number that has risen steadily over the past few years.2 Second, foreign investors hold around €575 billion in Italian public and private debt. About 80% of those investors are European investors, mostly asset managers but also banks and domestic households.3 French banks are the most exposed among European banking institutions.

Italian Debt to GDP percentage chart

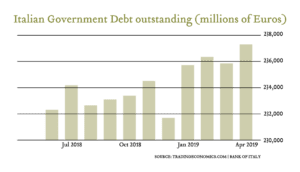

Italian Gov Debt Outstanding Chart

ITL Gov Securities by Holder Chart

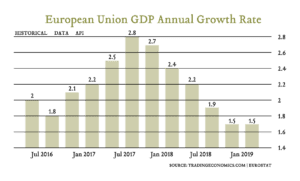

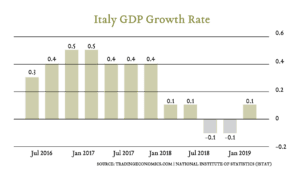

In a strong economy with robust domestic savings, these kinds of debt to GDP numbers would be of concern, but not unmanageable. Japan, after all, has a debt to GDP ratio of 234% but with a larger, stronger economy and very high savings. Even the US seems to be determined to run a deficit of a trillion dollars a year going forward through the magic of supply-side economics. However, the smaller Italian economy is slowing (shown below) and her savings rate is low (net saving is 0.7% as opposed to 10.6% in Germany).4 This puts pressure on the government’s balance sheet and will increase her borrowing further.

EU GDP Annual Growth Chart

Italy GDP Growth Rate Chart

One additional issue to consider when thinking about this debt is the rating of Italy by the world’s credit agencies. Most of these agencies have Italy on very low credit ratings, only a notch or two above high yield (junk), and on negative watch. Many of the banks have the same ratings as the sovereign with a large number of them on negative watch as well. If the government’s credit rating were to fall below investment grade i.e., below triple B, its bonds would no longer be eligible for holding among many investors. European banks, in particular, would no longer be able to use Italian government bonds as low risk weighted/high yielding assets for their reserves. Thus, not only would a series of downgrades generate losses on Italian and European bank balance sheets, but it would compromise the ability of the Italian government to raise funds going forward and, perhaps, even to participate in the ECB’s liquidity provision exercises.

|

Italian Credit Ratings: Long Term Rating Comparison |

|||

|

Agency |

S&P |

Moody’s |

Fitch |

|

Italian Ratings |

BBB |

Baa |

BBB |

As we said above, the Italian banking system owns a great deal of Italian government debt. These bonds are held as part of their reserves and banks have increased their purchases since the Financial Crisis, in part, encouraged by European and National authorities. Italian government bonds are both much higher yielding than other European government bonds and are zero risk weighted meaning they are free from capital requirements reflecting the view that they are free from rescheduling or default. As we know from the Greek crisis, this may or may not be true. In any case, they are not free of extreme price volatility. In the doom loop scenario, a crisis of confidence among investors around the Italian government pushes sovereign bond yields sharply higher in an environment of weak growth and rising deficits, undermining the already weak balance sheets of the domestic banks.

Late last year, The Bank of Italy highlighted this in their November 2018 Financial Stability Report.5 “The fall in prices for Italian government securities has caused a reduction in capital reserves and liquidity and an increase in the cost of wholesale funding. The sharp decline in bank share prices has resulted in a marked increase in the cost of equity. Should the tensions on the sovereign debt market be protracted, the repercussions for banks could be significant, especially for some small and medium-sized banks.” The Bank also noted that a reduction in the value of sovereign bonds on bank balance sheets reduces the liquidity which banks can obtain via Eurosystem refinancing operations.

While it can be said that Italian bond yields have dropped over the last few months, modestly improving the look of Italian bank balance sheets, this drop has been mostly due to the slowdown in the European economies, the need for the ECB to keep money rates low and the ECB’s need to maintain the provision of liquidity to banks via special targeted funding. This slowdown is negative for bank lending and profitability.

The past few years, the Italian banking system has made slow progress in improving its balance sheet exposure to non-performing loans (NPLs). A series of bank bailouts and forced mergers plus ECB enforced sales of assets have seen the banking system’s NPL exposure drop. However, most of the bond issues which bundle NPLs for sale or inject capital into Italian banks are being placed among Italian domestic investors keeping the insolvency risk further focussed in Italy. The current downturn in the economies of Italy and other European countries could derail the recent NPL progress. In addition, progress among the Italian banks has not been even, with some banks such as Banca Monte dei Paschi di Siena (the world’s oldest bank) and Banca Carige still having much to do despite several bailouts and capital injections (NPL ratios of 19% and 23% respectively) versus the two largest Italian banks, Intesa Sanpaolo and UniCredit (NPL ratios of 8.1% and 7.5%, respectively).5 The European Bank’s average NPL ratio is 3.1%.6 These banks and other medium-to-smaller institutions remain vulnerable.

Politics and Economics

In May 2018 a new government took office in Italy. Giuseppe Conte became Prime Minister backed by two populist, anti-immigration, and Eurosceptic parties. Matteo Salvini, leader of the Northern League, and Luigi Di Maio, leader of the Five Star Movement, became Deputy Prime Ministers of Italy, putting an anti-European spin on budget discussions. Their initial proposed budget was for a deficit of 2.4%, a figure well above the previous government’s 0.8% budget deficit plan. Given the slowing of the European and Italian economies and the already high level of Italian debt, the European Commission protested. (Bond investors also took this badly; see the spike in yields in the chart above at the end of last year.) They pointed out that nothing in the deficit was designed as an investment in the Italian economy (and so could be allowed under EU rules). In fact, the Commission argued that the main new spending plans, Universal Basic Income (UBI) for the unemployed, lowering the pension age to 60 and a flat tax proposal would likely only produce deeper deficits in years to come, especially as the new government also rolled back a scheduled VAT tax rise. The Commission argues that UBI will not be effective without an investment in training and retooling programs. Moreover, one struggles to think of another country which is reducing its pension age rather than extending it because, like Italy, most developed nations have an imbalance between younger taxpayers and a larger population of older citizens.

In December, the Commission and the Italian Government agreed on a 2.0% deficit. The proposals were modified, but concern remains as Italian growth for 2019 is projected to be just 0.1% by the Italian Finance Ministry. In fact, Italy’s project budget deficit for 2020 is forecast, by the European Commission, to be 3.1% breaching, for the first time since 2011, the EU 3% deficit limit. These wider deficits are likely to have a negative impact Italian sovereign and hence bank debt.

Nonetheless, the Italian government – backed by the Italian public who support its populist, Eurosceptic and anti-immigrant stance – is likely to persist in its desire to create budgets “for the poor” which break EU rules and undermine the Italian credit market. In May this year, at the European elections, the League and Matteo Salvini won over 34% of the vote, with the Five Star Movement taking another 17% giving more popular backing to their initiatives.

So, what are the risks to investors in this environment of larger government deficits, a weakened banking system and a slower economy?

Investor risks

- An internal credit crisis sparked by the current economic downturn could severely damage the ability of the Italian financial system to borrow and function. This would require further intervention from the ECB at a time when anti-centrist parties are in the ascendancy. The risk is not just domestic, however. With Italy being the 3rd largest economy in Europe and Italian bank credits widely held by European financial institutions as cheap capital, a European crisis that would test Euro and European credibility could result. As part of the doom loop, wider government deficits impact sovereign bond yields and hence bank balance sheets.

- An external financial crisis/risk aversion episode could also severely hurt the government spreads, then bank spreads and then domestic investors via losses on bonds and equities producing bankruptcies, forced mergers and equitization of debt.

Investor Conclusions

Enjoy your Italian vacation this summer – opera, art, sunshine – la dolce vita. But…

Given the current conditions, it would be prudent for investors to be careful with Italian credits, particularly those with weaker balance sheets including the Italian sovereign. It would be a worthwhile exercise for investors to look through the holdings of their Global and European bond funds where Italian credits may be included to lift the running yield of portfolios to offset negative to low-interest rates elsewhere, taking action where appropriate. Given the economic outlook for Italy and Europe in general, it would also be good for investors to look through their equity holdings seeking to prefer those companies with global rather than Italian domestic or European exposure only.

Sources: Italian National Institute of Statistics, European Banking Authority (EBA), European Banking Authority, Saving rate, European Banking Authority, EBA Risk Dashboard Q1 2019

Further reading:

Working Paper Series: Government debt and banking fragility: the spreading of strategic uncertainty. Russell Cooper, Kalin Nikolov European Central Bank

Financial Stability Reports No. 2 2018 and No. 1 2019, Banca D’Italia

European Banking Authority Risk Dashboard