June 6, 2025

Economic Commentary

Just five months into 2025, the global economic landscape has shifted from the cautious optimism observed at the start of the year. A flurry of tariff implementations throughout April and May has disrupted international trade. While some trade deals are emerging, the broader landscape remains uncertain, forcing businesses and governments worldwide to navigate unfamiliar waters. The markets will keep a close eye on the pace and scope of trade deals in the coming months – particularly on the 18 countries with which the U.S. has significant economic ties.

There has been an encouraging “step back from the brink” with de-escalation between the U.S. and China and a U.S.-UK trade agreement framework announcement. Financial markets reacted positively to these developments, recovering most of their losses from early April. Still, economic uncertainty remains elevated.

Dynamic trade policy is impacting business behavior and was evident in the Q1 GDP growth figures which came in well below expectations. Real GDP growth fell 0.3% in Q1, driven primarily by a surge in imported goods ahead of anticipated tariffs, which are a subtraction from GDP. Real final sales to private domestic purchasers, the sum of consumer spending and gross private fixed investment, increased 3.0 percent in Q1, reflecting the resilience of the US economy. Growth expectations have tracked trade policy announcements, with forecasters calling for a recession in the early weeks of April, then notching up growth expectations as trade tensions eased. Today, the consensus no longer calls for a recession in the next 12 months.

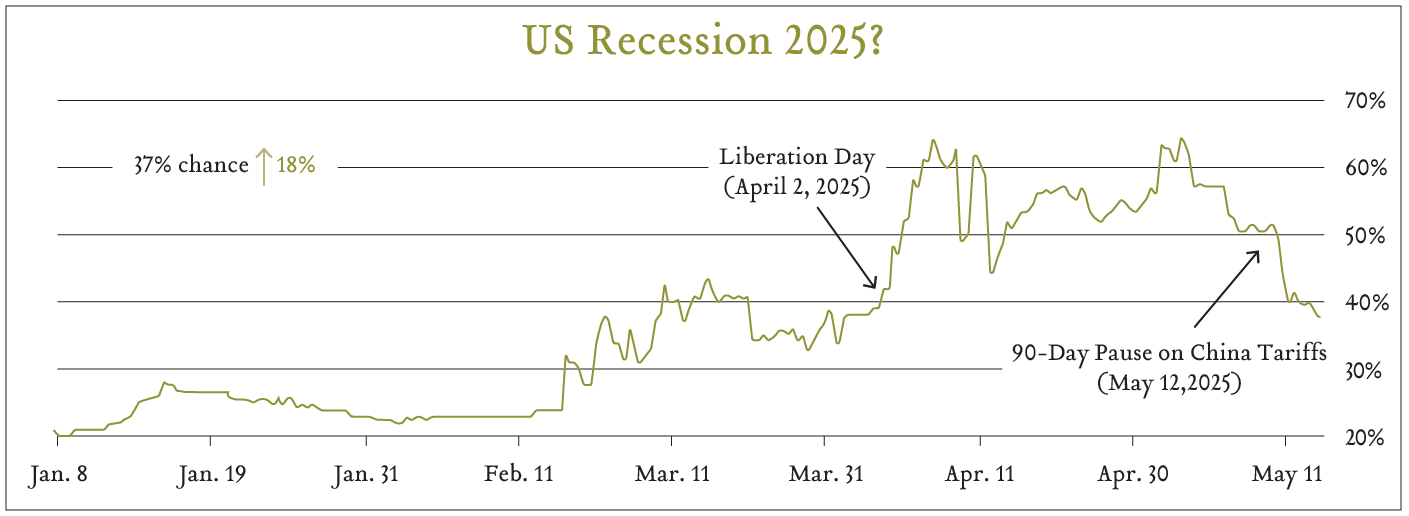

Some observers actually wager on whether or not the U.S. will enter a recession this year using online betting sites such as Polymarket. The graph below shows how the odds of a recession have changed throughout the year in response to policy announcements. The betting markets clearly saw increased tariffs as a risk to U.S. growth and currently assess continued expansion as likelier-than-not.

In addition to front-loading imports, importers now appear to be accepting lower margins on goods brought in since the new trade policies took effect. The U.S. Producer Price Index (PPI), fell by 0.5% in April 2025, defying market expectations of a 0.2% increase. This was the first decline in the PPI since October 2023 and the greatest drop since April 2020. The primary driver was a 1.6% decrease in margins for trade services, suggesting businesses, particularly in sectors like machinery and vehicle wholesaling, are choosing to absorb cost increases rather than pass them onto customers. If firms remain willing to shield consumers from rising costs, it would be positive for still-resilient consumer spending and may mitigate inflation pressures.

For investors, lower margins may not be a welcome development for earnings growth. To be fair, the 14.1% earnings growth expectations that were priced in at the beginning of the year may have been a bit optimistic. The market is now pricing in around 9% growth, with the largest markdowns in trade-impacted sectors like industrials, materials, and consumer discretionary. Market participants will be closely monitoring the passthrough effects of tariff costs and consumer strength – more certainty around trade would likely be a tailwind.

Any emerging slowdown in business activity hasn’t materialized yet in hiring, giving the Federal Reserve justification to keep interest rates stable at 4.25%–4.50% in May, the third consecutive meeting with no rate change. This was in line with expectations, as officials have adopted a wait-and-see approach while policy is in flux. April CPI inflation came in at 2.3% year-over-year. However, the April reading likely does not fully reflect price increases that may result from ongoing trade policy discussions. The April jobs report indicated 177,000 nonfarm payroll additions and a stable 4.2% unemployment rate. During the May FOMC press conference, Fed Chair Powell said that it was too early to determine whether inflation or unemployment will emerge as the greater concern and suggested that the Fed does not need to rush into adjusting interest rates. For the time being, the Fed is on the sidelines as it waits to see how the next few months will unfold. The market, for its part, has priced in two 0.25% cuts expected to take place in the latter half of the year.

Capital markets are forward-looking and, during periods of uncertainty, skittish. Establishing policy clarity, particularly with key trading partners, would help stabilize market expectations and reduce the risk of overreaction by investors or policymakers, including the Federal Reserve. The intersection of politics and economics is likely to continue to challenge investors’ discipline and ability to tune out headline risks. Many readers of this article have invested through multiple market cycles including the tech bubble, the global financial crisis, and the COVID-19 pandemic. The catalysts for market disruption may vary in each case, but the end result is much the same – markets normalized and investors who stuck with their investment plan benefited. We have no reason to anticipate that this cycle will be different than those of the past but are closely monitoring the rapidly evolving economic landscape. Thank you for the opportunity to serve on your behalf.