April 3, 2025

Economic Commentary

Market volatility made a sudden resurgence in the first quarter of 2025, unnerving many investors. While market participants have enjoyed relatively subdued volatility over the last two years, the experience of 2023 and 2024 was more the exception than the rule. In this article, we will explore the drivers of recent volatility and put the present condition within its proper historical context.

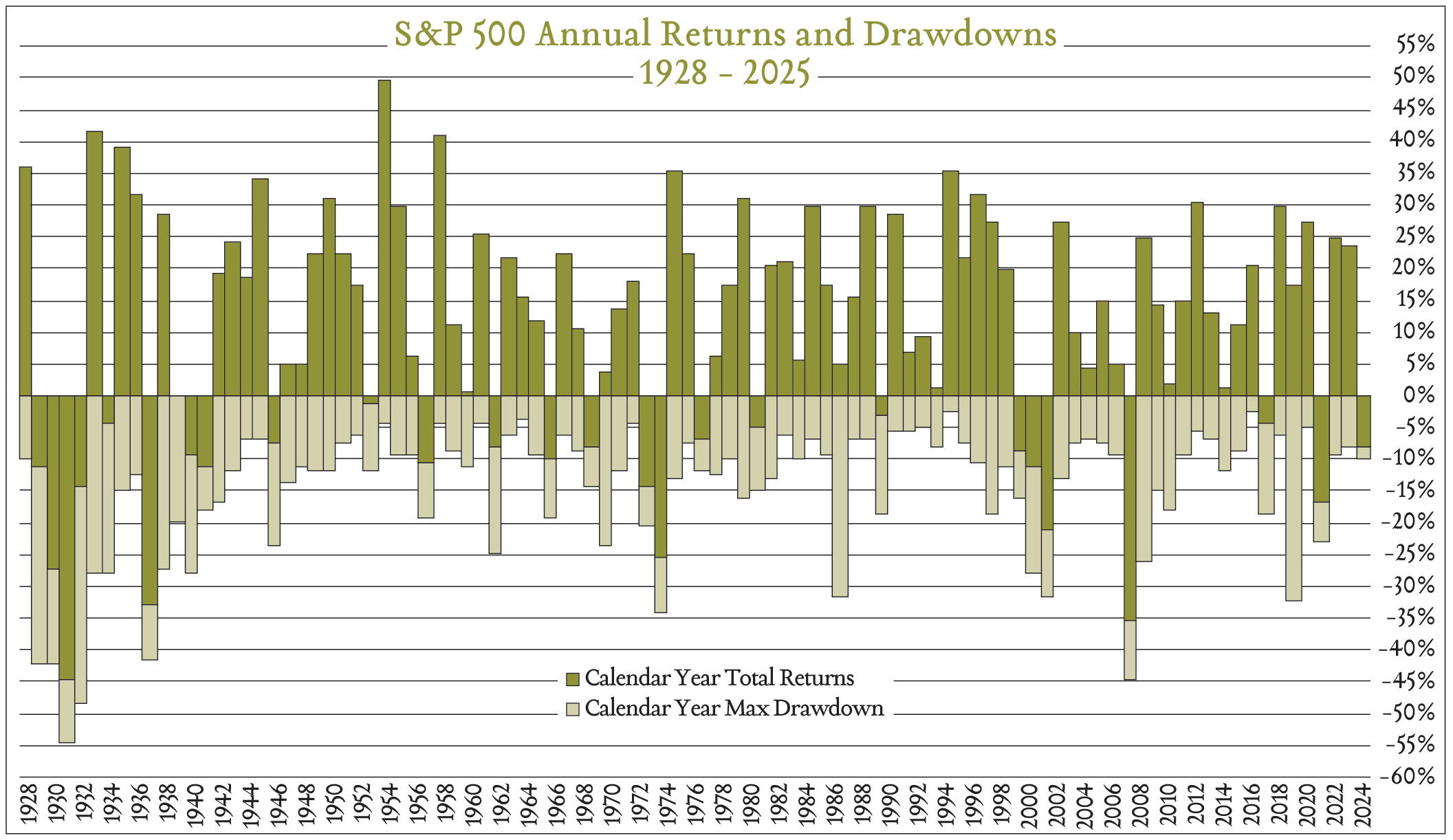

Whether we like it or not, volatility is an inherent characteristic of the stock market. Since 1928, the median drawdown of the S&P 500 index in a calendar year has been approximately 12%. This historical data underscores the idea that market fluctuations are not only normal but should be expected. As illustrated in the chart below, market drawdowns occur every year to varying degrees. Meanwhile, the median calendar year return has been 14.7% over the same period. During the first quarter of 2025 the S&P 500 experienced a correction, defined as a decline of 10% or more from a recent peak. While the decline was uncomfortable for investors, it is helpful to know that market corrections are actually quite common, occurring about once every two years historically. Moreover, bear markets, defined as a decline of 20% or more from a recent peak, occur about once every four years.

Understanding the Drivers of Volatility

Several factors have contributed to the recent spike in market volatility. Chief among these is the uncertainty surrounding US trade policy. The ongoing evolution of tariff proposals led to volatility in equity markets throughout February and March. US consumers, businesses, and investors are all facing a complex situation due to tariff announcements, postponements, exceptions, reversals, and retaliations.

To illustrate the dynamic nature of the trade policy landscape, consider the following:

- Canada and Mexico: Tariffs were announced in February, scheduled for early February, delayed, and then became effective in early March. Subsequently, 30-day exemptions were granted for some industries. Applicable rate is 25%, except for energy and potash fertilizer from Canada being assessed at 10%.

- China: 10% tariffs were announced in February and increased to 20% in March. Affecting approximately $430B in goods.

- European Union: Tariffs were announced in late February, and as of this writing the effective date has yet to be determined. The proposal consists of a 25% tariff on roughly $600B worth of goods.

- Steel and Aluminum: Tariffs were announced in February and became effective in March, with ongoing changes to exemptions and expansions.

- Autos: On March 27th, 25% tariffs on imported vehicle and vehicles parts starting April 3rd.

- Other Sectors: Policy changes or considerations are also in flux for copper, reciprocal actions, semiconductors, pharmaceuticals, timber, lumber, derivatives, and agricultural products.

Looking ahead, early April will be a crucial period as exemptions expire and further decisions on tariffs are considered.

So long as the real economy remains on solid footing, the short-term policy gyrations should do little to derail the long-term capital market outlook, so let’s take a look at how economic data is shaping up through the first quarter. A primary indicator of consumer strength, retail sales, advanced slightly in February, up 0.3% year-over-year after accounting for inflation. This report adds to the evidence that consumer spending is moderating amid tariff uncertainty and ongoing inflationary pressures but remains positive for the time being. As for inflation, the February CPI reading published in March showed inflation coming down slightly, landing at 2.8%. This beat analyst expectations and was below the 3% inflation reported for January, but does not reflect price increases that may result from recently announced tariffs. Lastly, The labor market continues to show resilience. In February there were 151K jobs added, which fell below expectations but represented an increase month-over-month. The unemployment rate ticked slightly higher to 4.1%, indicating some cooling amidst economic uncertainty.

Looking forward, economists are not as sanguine about the future and have marginally increased their estimates of the probability of a recession over the next twelve months. Beyond trade policy, several other factors are contributing to this pessimistic outlook. Federal government employment policies, for example, have the potential to impact a substantial number of direct and contract employees in 2025. While the impact may be relatively modest when put in the context of the overall labor market, it does introduce additional uncertainty.

Navigating Volatility: A Long-Term Perspective

In the face of volatility, it’s essential to maintain a long-term perspective and adhere to sound investment principles.

- Embrace Volatility as Normal: Recognize that volatility is a normal and expected part of investing. It is the trade-off investors accept in exchange for the potential for greater long-term returns.

- Focus on Your Investment Plan: Remember that your wealth management plan was created with market volatility in mind.

- Avoid Market Timing: Attempting to time short-term market fluctuations is generally not a successful strategy. It’s difficult to predict market movements consistently, and trying to do so can often lead to missed opportunities or losses.

- Maintain a Long-Term View: Focus on the long-term growth potential of the market. While short-term fluctuations can be unsettling, history has shown that the market has generally trended upward over the long run.

Policy uncertainty, evolving trade proposals, and various economic and political factors have driven increased market volatility in recent weeks. However, it’s crucial to remember that volatility is a normal part of investing. By maintaining a long-term perspective, and adhering to a well-crafted investment plan, investors can navigate these challenges and work towards achieving their financial objectives.